Where Does Your Money Actually Go?

We mapped every fee in a cross-border transfer. Three layers. Most providers only show you one.

Every cross-border payment provider charges you. That part isn’t surprising.

What’s surprising is how many of them won’t tell you exactly where the money goes.

That’s what MVP V2 is built to fix.

V1 was a simulation. Onboarding, add money, send, smart routing, receive — the whole flow, end to end, with no real money moving. A working prototype to prove the concept and make the case for the licenses we need to run real transactions.

It worked. But it had one thing backwards: you only saw the smart routing after you finished onboarding. The most useful part of the product was hidden behind a signup wall.

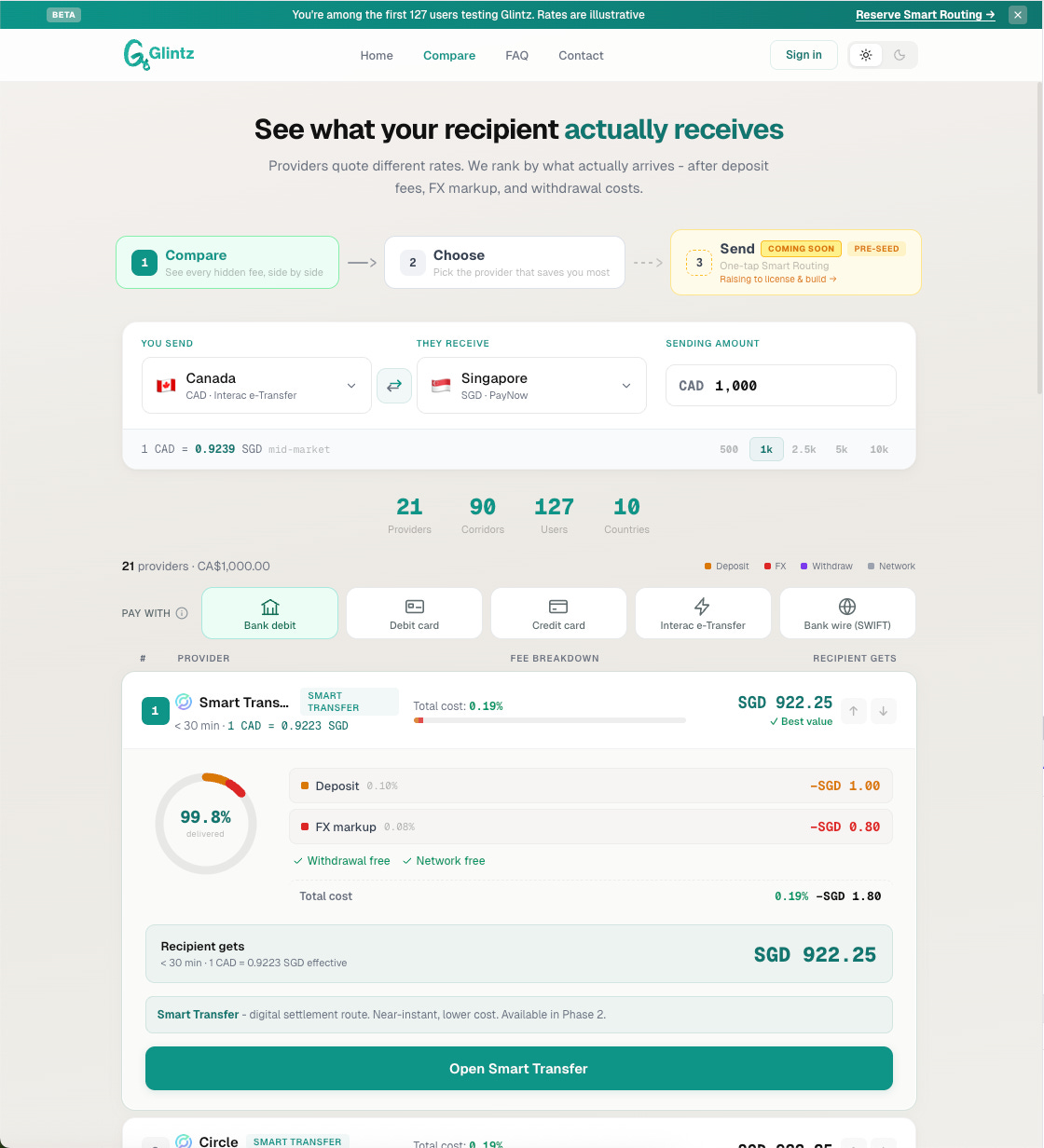

V2 flips it. Smart routing comes first. Before you create an account, before you hand over a single detail, you see every route — and every fee broken into three clear layers. Deposit. FX markup. Withdrawal.

So you know exactly where your money goes. Before you send

Three layers. That's where the money goes.

When you send money across borders, your transfer passes through three cost layers. Most providers lump them into one number and call it a "fee." Some hide them entirely inside the exchange rate and tell you the transfer is "free."

It's not free. Here's where the cost actually lives.

Layer 1: Deposit fee. The cost of getting your money into the system on the sending side. Interac e-Transfer, bank debit, credit card, Apple Pay, crypto. Each method has a different cost. Some providers absorb it. Some pass it through. Some bury it in the exchange rate and pretend the deposit costs nothing. A "zero fee" transfer that marks up the exchange rate by 2% just charged you $20 on a $1,000 send without showing a fee line.

Layer 2: Transfer fee. The cost of moving your money from one country to another. This is the core charge. The FX conversion, the provider's margin, the cost of operating across regulatory jurisdictions. Some providers show this as a flat fee. Some show it as a percentage. Some blend it into the exchange rate so you never see it at all. This layer is where most providers make their real money, and where the biggest variance between providers lives.

Layer 3: Withdrawal fee. The cost of delivering money on the receiving side. Bank deposit, mobile wallet, cash pickup. Each delivery method costs differently. PayNow in Singapore is nearly free. A bank wire to a rural branch in the Philippines costs more. Cash pickup at a physical location has its own fee. The delivery method changes the final math more than most people realize.

Three layers. When you see them side by side across 14 providers, the numbers tell a story that a single "fee" never could.

And that story gives you leverage, not just a ranking. When you see the deposit fee, you might switch from a credit card to a bank debit and drop $15 from the cost immediately. When you see the transfer fee, you understand why one corridor is expensive and another isn't, and you stop assuming the "free" provider is actually free. When you see the withdrawal fee, you realize that switching the delivery method from bank wire to mobile wallet might put more money in your recipient's hands than switching providers entirely. One number tells you the price. Three layers tell you where the price lives, and that changes what you can do about it.

Where stablecoins fit

Traditional cross-border transfers move through correspondent banking networks. Your money hops from your bank to a local clearing system, through one or two intermediary banks, across SWIFT, into the destination country's clearing system, and finally into the recipient's account. Every hop takes a cut. Every hop takes time.

Stablecoins change the plumbing.

A stablecoin transfer moves value on a blockchain. No intermediary banks. No SWIFT. No correspondent chains. The transfer fee drops because the infrastructure is cheaper to operate. Settlement that used to take 1-3 business days can happen in minutes.

This doesn't mean stablecoins are always the cheapest option. Deposit costs depend on how you buy the stablecoin. Withdrawal costs depend on how the recipient converts it back to local currency. The three-layer breakdown still applies. But the transfer layer, the middle piece, gets dramatically cheaper when you remove the banking chain.

Circle's USDC just overtook Tether's USDT in transaction volume for the first time since 2019, hitting $6.2 trillion in monthly volume. Mastercard paid $1.8 billion for BVNK to add stablecoin rails to their payment infrastructure. Sokin launched a hybrid platform where businesses can send money through fiat or stablecoin rails, whichever is cheaper for the corridor.

Stablecoins aren't replacing traditional transfers. They're becoming another rail. Another option in the comparison. Another row in the table that might save you money depending on your corridor, your amount, and your delivery method.

Glintz’ MVP V2 includes stablecoin providers alongside traditional ones. Same three-layer breakdown. Same ranking by what actually arrives. The best option might be a traditional provider for one corridor and a stablecoin-based one for another. You shouldn't have to know which rails your money travels on. You should just see the cost and the result.

How it works: Compare. Choose. Send.

Glintz works in three steps.

Step 1: Compare. This is live now. You pick your send country, receive country, and amount. Glintz pulls fees and rates from the sources we can surface today, decomposes each provider's cost into the three layers, and ranks by what actually lands in your recipient's account. We're expanding our data sources as we go, and every new one makes the picture sharper.

Step 2: Choose. You pick the provider that fits what you need. Maybe it's the cheapest option. Maybe it's the fastest. Maybe it's the one that delivers to a mobile wallet instead of a bank account. The fee breakdown gives you enough information to make that choice with confidence instead of guessing.

Step 3: Send — coming soon. Right now, Glintz redirects you to the provider you chose. You complete the transfer on their platform. In the next phase, we want to enable one-tap smart routing directly through Glintz. You set your priorities, speed or cost or reliability, and the system picks the best provider and executes the transfer for you.

But sending money on behalf of users isn't something you can just build and ship. It requires proper licensing.

In Canada, that means a Money Services Business (MSB) registration with FINTRAC. In the US, it's state-by-state Money Transmitter Licenses, plus federal FinCEN registration. In the EU, it's an Electronic Money Institution (EMI) license under the Payment Services Directive. Every country has its own version.

These licenses exist for a reason. They protect the person sending money. They require companies to hold client funds separately from operating funds, so your money is safe even if the company has a bad quarter. They mandate anti-money laundering checks, so the system can't be used to move illegal funds. They require transaction reporting, so regulators can spot problems before they become crises.

Without a license, a company is just moving money and hoping nothing goes wrong. With a license, there are rules, audits, consumer protections, and accountability.

That's why Step 3 says "coming soon." We're raising funding to secure the proper licensing, build the compliance infrastructure, and launch smart routing the right way. Not fast. Right.

The fee transparency fight

The G20 set a target to bring cross-border payment costs below 1% by 2027. The global average is still 6.5%. Even digital-only remittances sit around 5%. A 2023 Wise study found 92% of European banks still hide their FX fees in inflated exchange rates.

Wise proved that transparency wins. £145 billion in annual volume. £1.2 billion in revenue. 15.6 million customers. All built on showing people the real cost.

But Wise is one provider, showing one price. Their own.

Glintz shows you everyone’s. Broken into three layers. Ranked by what actually arrives.

That’s the difference between a transparent provider and a transparent platform.

Who else is building this way

Multi-rail, multi-provider routing won.

The infrastructure layer figured out that no single provider has the best price on every corridor, every day, in every direction. So the architecture that wins is the one that scores them all and picks in real time.

Billions of dollars went into building that architecture. None of it for consumers.

The person sending $1,200 SGD to her family in Vancouver on a Tuesday night still gets a Google search and three browser tabs. Not because the technology doesn’t exist. Because nobody bothered to point it at her.

That’s the gap. That’s what we’re building.

Sources:

Wise FY2025 — £145.2B cross-border volume (~$185B), £1.2B revenue (~$1.5B), 15.6M active customers. Wise Owners

G20 cross-border cost target — ≤1% global average by 2027 (FSB says target unlikely to be met). FSB Progress Report 2025

Average remittance cost — 6.49% global average for sending $200 (Q1 2025). World Bank Remittance Prices Worldwide

92% of European banks hide FX fees — 2023 study of 25 European banks. Wise CBPR2 Report

Mastercard acquires BVNK — $1.8B, March 17, 2026. Mastercard Press Release

Nuvei taken private — $6.3B by Advent International, announced April 2024, closed November 2024. PR Newswire

Airwallex — $8B valuation, $330M Series G, >$1B annualized revenue (December 2025). Airwallex Newsroom

Payoneer FY2025 — $1.053B revenue, 8% YoY growth. Payoneer Investor Relations

Rapyd — $1.01B total raised, $4.5B valuation (Series F, March 2025; down from $10B peak in 2021). Calcalist

Spreedly — $60B+ annualized GMV, $82.8M raised. Crunchbase

Primer — $73.9M raised, $425M valuation, J.P. Morgan Payments integration (March 2025). Fintech Global

Modern Treasury — $183M raised, $2B valuation (March 2022). BusinessWire

Gr4vy — $27.2M total funding (Series A + extension). TechCrunch

Payment orchestration market — $3.13B in 2026, 18.3% CAGR through 2031. Mordor Intelligence

PayTech M&A activity 2025 — 610 total deals tracked. Edgar, Dunn & Company

Circle USDC overtakes USDT in transaction volume — first time since 2019, $1.26T USDC processed in February 2026. CoinDesk

Sokin launches stablecoin capabilities — March 17, 2026, with Genpaid acquisition. PR Newswire